African countries make up a very small share of China’s investment, global trade and Chinese banks’ loan portfolio, but Chinese construction companies did roughly a third of their business in Africa in 2015.

We first investigate the role that economic engagement with African countries plays for China. China’s economic engagement with the world accelerated rapidly after the country joined the World Trade Organization in 2001, and Foreign Direct Investment is no exception.

Foreign Direct Investment (FDI)FDI is a form of investment that is made with the goal of having a long-term say in the management of an enterprise operating outside of the country of the investor. The investment an be made by buying a company in the target country or by expanding the operations of an existing company into the target country. For most definitions, some degree of equity capital ownership is required to qualify as a foreign direct investor. The International Monetary Fund suggests a minimum of 10% of equity ownership. Forms of investment which are classified as FDI are equity capital, reinvestment of earnings and the provision of loans between parent and affiliate enterprises. See here for a formal definition.

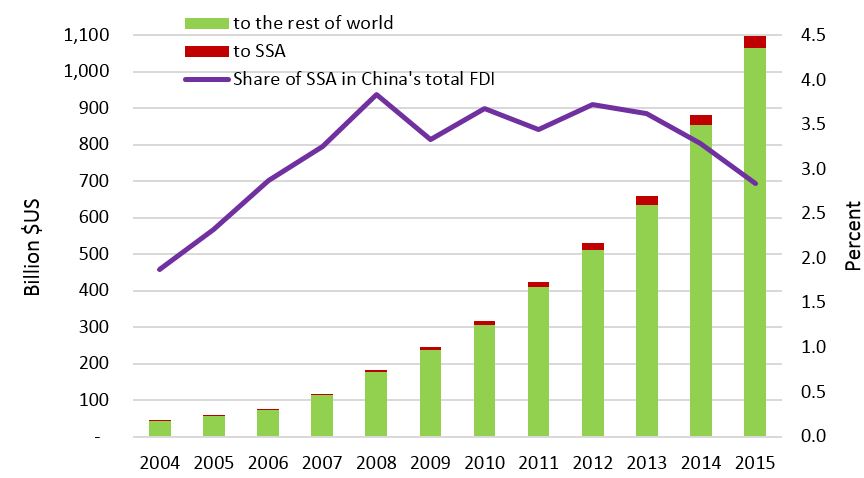

Since 2001, the Chinese government incentivised domestic investment abroad through a ‘go-out’ policy. This was motivated by large amounts of foreign reserves accumulated by China, the domestic need for raw materials and aimed to improve firms’ competitiveness with Western multinationals. Figure 1 illustrates this rapid increase in total Chinese FDI stocks worldwide and the share of it going to countries in Sub-Saharan Africa. The purple line shows that African countries only account for a very small share, about 3 % in 2015, of Chinese global investment. In comparison, more than half of Chinese investment is directed towards Hong Kong, while Europe, South America and Asia all receive more FDI than Sub-Saharan Africa. We use official statistics provided by China’s Ministry of Commerce and National Bureau of Statistics for data on Chinese FDI, and from the United Nations Conference on Trade and Development (UNCTAD) for other countries’ investment into Africa. We consider this Chinese data the best available since it only includes realised investments as compared to the much larger value of planned investments. It is also relatively reliable since the Chinese government requires all firms to regularly report on their investments abroad. However, this data does miss smaller projects under $10 million value and investments going through offshore tax havens.

FDI Stocks vs. FlowsFDI stocks measure the total level of foreign direct investment at a given point in time. The outward FDI stock of a country is the value of FDI that domestic investors hold in foreign countries. The inward FDI stock of a country is the value of FDI held by foreign investors in the reporting country.FDI flows record the value of foreign direct investments made during a given period of time. Outward FDI flows of a country are transactions that increase the stock of FDI held by domestic investors in foreign countries. Inward FDI flows of a country are transactions that increase the stock of FDI held by foreign investors in the reporting country.See here and here for formal definitions.

Figure 1: China's FDI to Africa and the Rest of World - Stocks

Source: Authors' calculations using data from Table of "China's Outward FDI Flows by Country and Region" in China Commerce Yearbook (various years), published by Ministry of Commerce (MOFCOM) - click here. The data is same as from China Statistical Yearbook: "Oversea Direct Investment by Countries or Regions" - click here; and UNCTAD Bilateral FDI Statistics - click here.

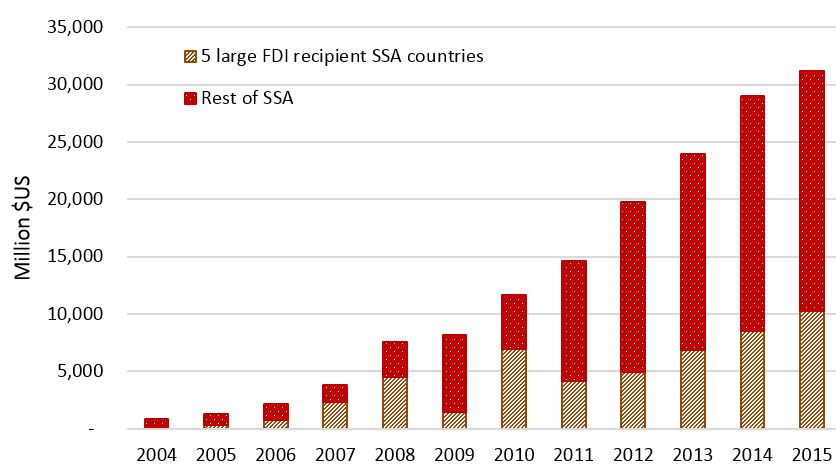

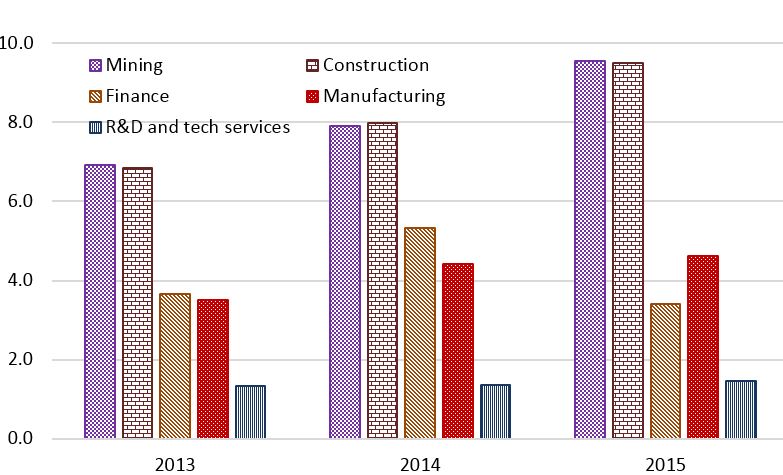

Further examination reveals that Chinese investment in the region is starting to diversify, both in terms of geography and sector. The growing red bars in Figure 2 show that, within Africa, the role of the primarily resource-rich large recipients of FDI (Democratic Republic of Congo (DRC), Nigeria, South Africa, Sudan and Zambia) in Chinese FDI has been decreasing in recent years, compared to other African economies. And while mining and construction continue to be the top two target sectors for Chinese FDI in African countries, Chinese FDI in African manufacturing has been increasing recently, as the red bars in Figure 3 demonstrate. This contrasts with some of the academic literature identifying natural resources and poor governance as determinants of Chinese investment (e.g. Kolstad and Wiig 2011, Ramasamy et al 2012, Zhang et al 2013, Ross 2015), but is supported by more elaborate studies showing that Chinese FDI follows typical profit-seeking motives, is determined largely by firm-specific advantages and market access and has been converging with patterns of engagement by Western high-income countries (Chen et al 2015, Sindzingre 2016, Seyoum and Lin 2015).

Figure 2: China's FDI in Africa, Total Africa, Large Recipient Countries and the Rest of Africa - Stock

Source: Authors' calculations using data from Table of "China's Outward FDI Flows by Country and Region" in China Commerce Yearbook (various years), published by Ministry of Commerce (MOFCOM) - click here. The data is same as from China Statistical Yearbook: "Oversea Direct Investment by Countries or Regions" - click here; and UNCTAD Bilateral FDI Statistics - click here.

Figure 3: Top Five Sectors in China's FDI Stocks in Africa (Billion $US)

Source: Statistical Communique on China's Foreign Direct Investment (MOFCOM 2017) - click here. Note: The data is for whole Africa including North Africa, as the data cannot be separated for SSA countries.

Chinese investment, trade, contracted construction projects and loans often are interconnected, or “bundled” (Kaplinsky and Morris, 2009). For example, Chinese FDI in the mining or construction sectors often goes together with loans from the Chinese government to African governments, which in turn contract Chinese firms to build infrastructure or extract resources. The repayment of these loans in turn is often tied to exports of commodities from African borrowers to China. Hence, it is instructive to put Chinese investment in Africa into context with these other types of Chinese engagement with the continent.

In monetary terms, trade is the most important channel of Chinese engagement with the world as well as with African countries, as data from the United Nations Trade Statistics Database (UN COMTRADE) shows. Trade flows with African countries dwarf Chinese investment into the continent: while China exported goods of more than $76 billion value to Sub-Saharan Africa in 2015, the total stock of FDI in the region amounted to only $31 billion in 2015 (see Figure 2). However, like investment, trade with Africa represents a very small share of China’s global trade, about 3.5 % of Chinese exports and 4 % of imports into China in 2015. In contrast, Africa accounts for a large share of construction projects abroad won by Chinese firms, representing nearly a third of the value of global contracts that Chinese companies engage in in 2015. This construction activity does appear to create jobs. Sautman and Yan (2015) find that 87 % of employees in Chinese construction projects are local. In terms of loans, China’s influence globally has been increasing both unilaterally through its largest banks (the China Development Bank and the Export-Import Bank of China), and multilaterally through participation in funds such as the Asian Infrastructure Investment Bank. However, the volume of loans going to African governments and state-owned enterprises is small, amounting to only $86.9 billion between 2000-2014 compared to $684 billion of assets invested overseas by China’s two biggest banks. Most loans are made above market interest rates and hence cannot be considered concessional, though they may be cheaper than finance available from other sources.

Overall, African countries make up a very small share of China’s global trade, investment and loan portfolio, but represent a large share of China’s construction projects overseas. Therefore, a slowdown of growth in Africa would likely have a minimal effect on the Chinese economy, thought it would deal a significant blow to Chinese construction companies that are active in Africa.