African countries are much more reliant on trade with China than on Chinese FDI, though Chinese FDI on the continent has been increasing and diversifying towards less resource-rich and high-growth countries recently.

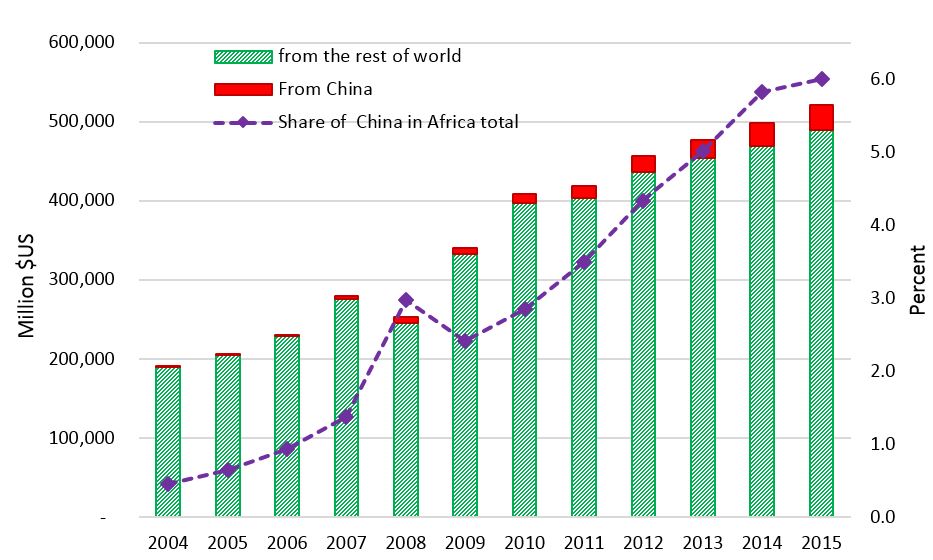

We next look at the importance of Chinese activity to countries in Sub-Saharan Africa (SSA). At the same time that China opened up to the global economy in the early 2000s, many African economies experienced a growth renaissance. The average growth of GDP in 38 Sub-Saharan African economies between 2000 and 2015 was 4.9 %, with many resource-poor economies performing above average. This growth spurt was accompanied by a large increase in incoming FDI, as the bars in Figure 4 demonstrate. As the dashed line in the same figure shows, the share of Chinese FDI as a share of total FDI stock in Africa increased steadily in this period, from less than 1 % in 2004 to 6 % in 2015. Nevertheless, this share is still small in relative terms.

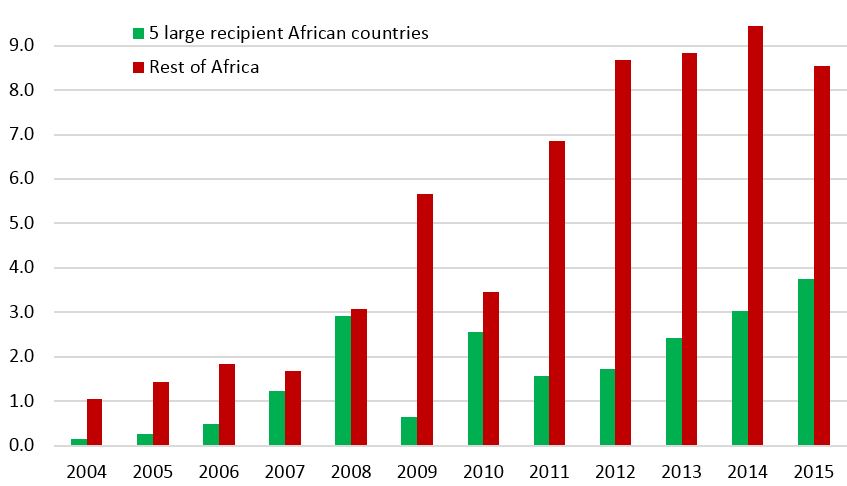

When breaking the data down into Africa’s five largest recipient countries of FDI (DRC, Nigeria, South Africa, Sudan and Zambia) and the rest of Sub-Saharan Africa, we see a more interesting pattern. Until about 2008, Chinese investment patterns in Africa mirrored investment patterns by the rest of the world, since Chinese FDI as a share of total FDI stocks was similar in the large recipient countries and in the rest of SSA (Figure 5). However, since 2009 China has become a more important investor in countries outside the top five recipients, with its FDI representing 8-9 % of total FDI stocks in these countries in recent years. This indicates that China is diversifying its investments towards countries outside the large recipients and that this diversification is happening more rapidly than for other countries’ investments.

Figure 4: Total FDI Stocks in Africa from China and the Rest of the World and Share of China

Source: UNCTAD (2017) - click here.

Figure 5: Share of China's FDI in Africa Total Inward FDI Stocks, Total Africa, Large Recipient

Source: Authors' calculations using data from Table of "China's Outward FDI Stocks by Country and Region" in China Commerce Yearbook (various years), published by Ministry of Commerce of the People's Republic of China. Note: The five large FDI recipient countries are DRC, Nigeria, South Africa, Sudan and Zambia.

To put the numbers on FDI into perspective, we also look at trade. African countries appear much more reliant on trade with China than on Chinese investment. After a period of rapid increase, exports to China in 2015 represented roughly 20 % of total exports for SSA, and imports from China accounted for about 25 % of total imports into SSA in the same year. There is some evidence that the increased import penetration by Chinese products may have had negative effects on African producers and intra-African trade (Edwards and Jenkins 2015a, 2015b), though it might also have pushed some domestic producers to innovate (Sonobe, Akoten and Otsuka 2009, Abebe et al 2018). Unfortunately, data limitations preclude us from looking at Chinese construction activity and lending in a similar way.

In summary, the importance of Chinese FDI for African economies is much smaller than the role of trade flows, although Chinese investment has recently gained a more prominent role in African countries outside the top five recipients.

a) Chinese investment in Africa's fastest growing economies

While GDP in Sub-Saharan African countries grew by close to 5 % on average between 2000-2015, 16 countries had even higher growth rates. This sub-section asks whether it is possible that Chinese investment played a role in driving this growth.

We find that domestic and foreign investment combined consistently grew at a faster rate than GDP in most high-growth countries between 2000-2015, in resource-rich and resource-poor countries alike. This indicates that investment was at least a proximate driver of growth for these countries and that the high GDP growth observed was not necessarily related to commodity booms. Between 2004-2015, total FDI represented an average share of 12.4 % in total investment, but this share varied a lot across countries (between 60 % for Sierra Leone and negative, that is FDI outflows, from Angola).

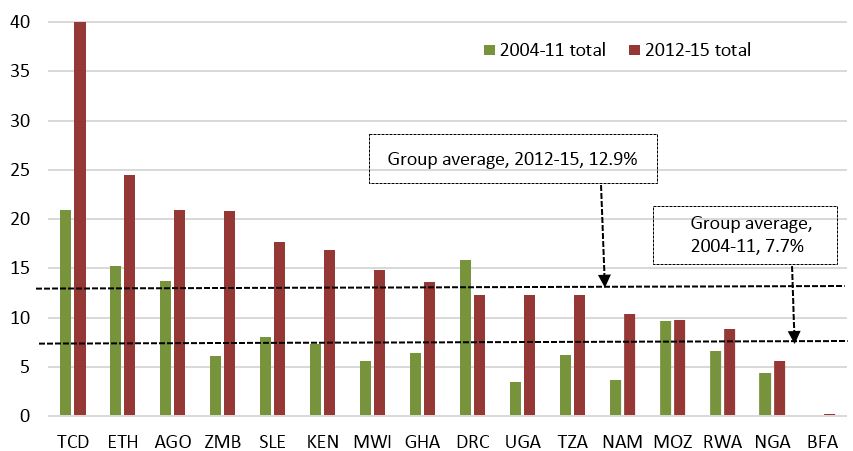

We also find that Chinese investment inflows increased faster than total FDI flows from all countries in all but two of the high-growth countries when comparing the time periods 2004-2011 and 2012-2015. Nevertheless, the share of Chinese FDI inflows in total FDI inflows is still small for most high-growth countries. As the red diamonds in Figure 6 show, this share has been below 15 % in 2012-2015 for all high-growth countries except Kenya and Chad, where it is around a quarter.

Figure 6: FDI Inflows in 16 High Growth Countries from the World and China, 2012-2015 Aggregation

Source: Authors' calculations using data from UNCTAD (2017)

To put these numbers into perspective, we also look at the role of Chinese construction projects in total investment in a country. The share of Chinese contracted construction projects in total investment increased in 15 out of the 16 high-growth countries from 2004-2011 to 2012-2015, with the average share rising from 7.7 % to 12.9 % between these periods. It also appears that countries with high total investment growth in recent years exhibit higher shares of Chinese construction in total investment.

Overall, the evidence indicates that investment has played a key role in the growth of Africa’s fastest-growing economies, and that this investment is not limited to natural resources. Although Chinese FDI was not a large share of investment in most high-growth countries, its role in financing investment has increased more rapidly in the high-growth countries than in the rest of Africa in recent years.

b) Chinese investment in African manufacturing

It is well understood that manufacturing has the potential to create jobs and stimulate economic growth through structural change (McMillan and Rodrik 2011). And while the manufacturing sector in African economies is still small, China’s recently growing investments in the sector raises the question whether China’s engagement could have a transformative effect on the continent. This sub-section therefore focuses on Chinese investment in manufacturing in African countries and the extent to which these investments are linked to the local economy.

Special Economic Zones (SEZ) have been a feature of China’s outward economic strategy and its domestic growth. Five SEZs in Sub-Saharan Africa were approved in 2007. While most of these zones are not yet at capacity and have not yet realised their committed levels of investment, they seem to have created substantial local employment. Data for three zones in Zambia, Ethiopia and Nigeria indicate that there are six local employees for every Chinese worker. However, supply linkages and transfer of know-how to local companies so far appears to be limited outside of Nigeria (Brautigam and Tang 2014).Special Economic Zones (SEZs)Special Economic Zones are areas that provide economic incentives to businesses located within the zone with the aim of attracting foreign or domestic businesses. The incentives provided vary but can include more liberal economic laws than in the rest of the country, better public services (e.g. customs and licensing) and infrastructure, fiscal incentives (e.g. subsidies or tax incentives) and others. While the term encompasses many different types of SEZs, SEZs are most often set up to attract FDI, promote exports or support industrialisation.See PEDL Synthesis Paper Series No. 1 for a comprehensive discussion.

Brautigam, Tang and Xia (2017) provide additional evidence from interviews in four African countries with 90 Chinese firms in total that are active in entry-level sectors such as leather processing, textiles, plastic goods, agro-processing. They find that more than a quarter of these firms had originally come as traders to the African countries they were active in and only later decided to invest in production to take advantage of access to local markets. A large majority of these firms sells their products primarily on local markets, except for firms active in Ethiopia in the textile and leather sectors that target export markets. Firms that focus on the local market report that they are primarily competing with imported goods and foreign firms in the countries, instead of domestic firms. These firms can also benefit from trade-protectionist policies by host countries because they are located in the country. In contrast, exporters aim to take advantage of regulations that allow exporters based in Sub-Saharan Africa to gain preferential access to the US and European markets, such as the African Growth and Opportunity Act (AGOA) with the USA and the Everything But Arms (EBA) deal with the European Union.

Transfer of knowledge to local firms mainly occurs through the training of local workers, as Brautigam, Tang and Xia (2017) find. Only few joint ventures, technical partnerships and backward linkages, where local firms engage with Chinese suppliers, were reported. Nevertheless, Chinese firms procure a significant share of inputs from local firms and have thus pushed some local companies to improve machinery and processes to meet quality standards. Abebe et al (2018) investigate linkages for the Ethiopian case, using a study design that relies on exogenous placement and timing of new FDI plants between 1997-2013. While they are not able to separate the effects of Chinese FDI because of too few firms in Ethiopia, evidence on FDI generally in Ethiopia indicates positive effects not only in the form of knowledge transfers via labour flows, but also through communication between firms and linkages in the supply chain. Their study also finds that the Chinese firms in Ethiopia pay higher wages than domestic firms and, in line with Brautigam, Tang and Xia (2017), that they mainly hire local labour and source most of their inputs locally.

Overall, the Chinese firms interviewed in Brautigam, Tang and Xia (2017) were optimistic about future production opportunities in African countries, compared to rising production costs, overcapacity and a saturated market in China. This is echoed by the Chinese government, which officially committed to supporting African industrialisation at the Forum on China Africa Cooperation in December 2015. While Chinese investment in African manufacturing is still small, the evidence in this section indicates that there is potential for African economies to benefit from knowledge transfers and employment growth.